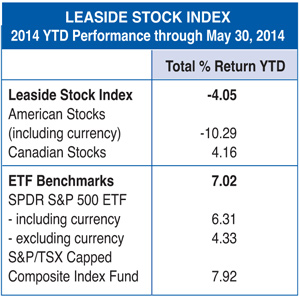

As I write this half way through June the S&P 500 on a daily basis seems to be setting all-time record highs and is up almost 7 percent through the first half of 2014. Yet one of the U.S. stocks in the Leaside Stock Index — Best Buy (BBY) — continues its bumbling ways, down 25.2 percent year-to-date. While its recent performance holds promise, at some point you have to cut your losses. In the June edition of the paper I wondered whether Walmart (WMT) would make a better holding for the LSI given the sorry state of Best Buy’s business. However, since Walmart won’t be eligible until late next year I concluded that since a lot can happen in 18 months I wasn’t going to make any rash moves altering the portfolio. It’s one month later and I’ve changed my mind. Although I still might leave things doing well enough alone it doesn’t hurt to consider some alternatives. There’s a handful of possibilities that could do the trick. Unfortunately, some of the more obvious candidates are Canadian stocks — Second Cup (SCU.TO) and Pizza Pizza (PZA.TO) — and we’re in need of a U.S. stock. No matter. I’ve put my thinking cap on and come up with three possibilities: 1. TJX Companies (TJX) is a multi-concept discount retailer based in Columbus, Ohio, that operates Winners, HomeSense and Marshalls here in Leaside. Turning its inventories 12 times a year provides it with significant operating cash while keeping customers coming back to see what’s new on the racks throughout the store. CEO Carol Meyrowitz is one of the best executives in retail. A $10,000 investment in TJX 10 years ago is worth $46,450 today compared to $15,410 for Walmart. 2. RPM International (RPM) is the parent company of Tremco, a manufacturer of paints and sealants located at 220 Wicksteed Ave. RPM acquired Tremco from B.F. Goodrich in 1997 for $230 million. Although RPMs performance hasn’t been as stellar as TJXs, a $10,000 investment a decade ago is still worth $29,345 today; more than $8,000 greater than the S&P 500. 3. Imperial Oil (IMO.TO) is a bit of an asterisk. Although Calgary-based and trading on the Toronto Stock Exchange, it is 70 percent owned by Exxon Mobil (XOM), the world’s largest oil and gas company. Imperial Oil owns 25 percent of the Syncrude joint-venture at the Athabasca Tar Sands in Alberta which produces approximately 100 million barrels of oil annually. Although great for the Alberta economy it certainly does a number to the landscape. Of the three stocks XOM would be my least favorite. So, should Best Buy be sent packing for one of these other stocks? While I’d love to substitute TJX, which is also down in 2014, Best Buy has shown enough in the past month to stay in the game. As long as it doesn’t drop too far from where it is now I think it makes sense to remain patient. Stocks are somewhat expensive at the moment providing inves- tors with few value plays. Best Buy’s June 10 announcement that it was increasing its quarterly dividend for the first time in two years is a good indication its turnaround is working. No, Best Buy shouldn’t be sent packing — just yet.

As I write this half way through June the S&P 500 on a daily basis seems to be setting all-time record highs and is up almost 7 percent through the first half of 2014. Yet one of the U.S. stocks in the Leaside Stock Index — Best Buy (BBY) — continues its bumbling ways, down 25.2 percent year-to-date. While its recent performance holds promise, at some point you have to cut your losses. In the June edition of the paper I wondered whether Walmart (WMT) would make a better holding for the LSI given the sorry state of Best Buy’s business. However, since Walmart won’t be eligible until late next year I concluded that since a lot can happen in 18 months I wasn’t going to make any rash moves altering the portfolio. It’s one month later and I’ve changed my mind. Although I still might leave things doing well enough alone it doesn’t hurt to consider some alternatives. There’s a handful of possibilities that could do the trick. Unfortunately, some of the more obvious candidates are Canadian stocks — Second Cup (SCU.TO) and Pizza Pizza (PZA.TO) — and we’re in need of a U.S. stock. No matter. I’ve put my thinking cap on and come up with three possibilities: 1. TJX Companies (TJX) is a multi-concept discount retailer based in Columbus, Ohio, that operates Winners, HomeSense and Marshalls here in Leaside. Turning its inventories 12 times a year provides it with significant operating cash while keeping customers coming back to see what’s new on the racks throughout the store. CEO Carol Meyrowitz is one of the best executives in retail. A $10,000 investment in TJX 10 years ago is worth $46,450 today compared to $15,410 for Walmart. 2. RPM International (RPM) is the parent company of Tremco, a manufacturer of paints and sealants located at 220 Wicksteed Ave. RPM acquired Tremco from B.F. Goodrich in 1997 for $230 million. Although RPMs performance hasn’t been as stellar as TJXs, a $10,000 investment a decade ago is still worth $29,345 today; more than $8,000 greater than the S&P 500. 3. Imperial Oil (IMO.TO) is a bit of an asterisk. Although Calgary-based and trading on the Toronto Stock Exchange, it is 70 percent owned by Exxon Mobil (XOM), the world’s largest oil and gas company. Imperial Oil owns 25 percent of the Syncrude joint-venture at the Athabasca Tar Sands in Alberta which produces approximately 100 million barrels of oil annually. Although great for the Alberta economy it certainly does a number to the landscape. Of the three stocks XOM would be my least favorite. So, should Best Buy be sent packing for one of these other stocks? While I’d love to substitute TJX, which is also down in 2014, Best Buy has shown enough in the past month to stay in the game. As long as it doesn’t drop too far from where it is now I think it makes sense to remain patient. Stocks are somewhat expensive at the moment providing inves- tors with few value plays. Best Buy’s June 10 announcement that it was increasing its quarterly dividend for the first time in two years is a good indication its turnaround is working. No, Best Buy shouldn’t be sent packing — just yet.